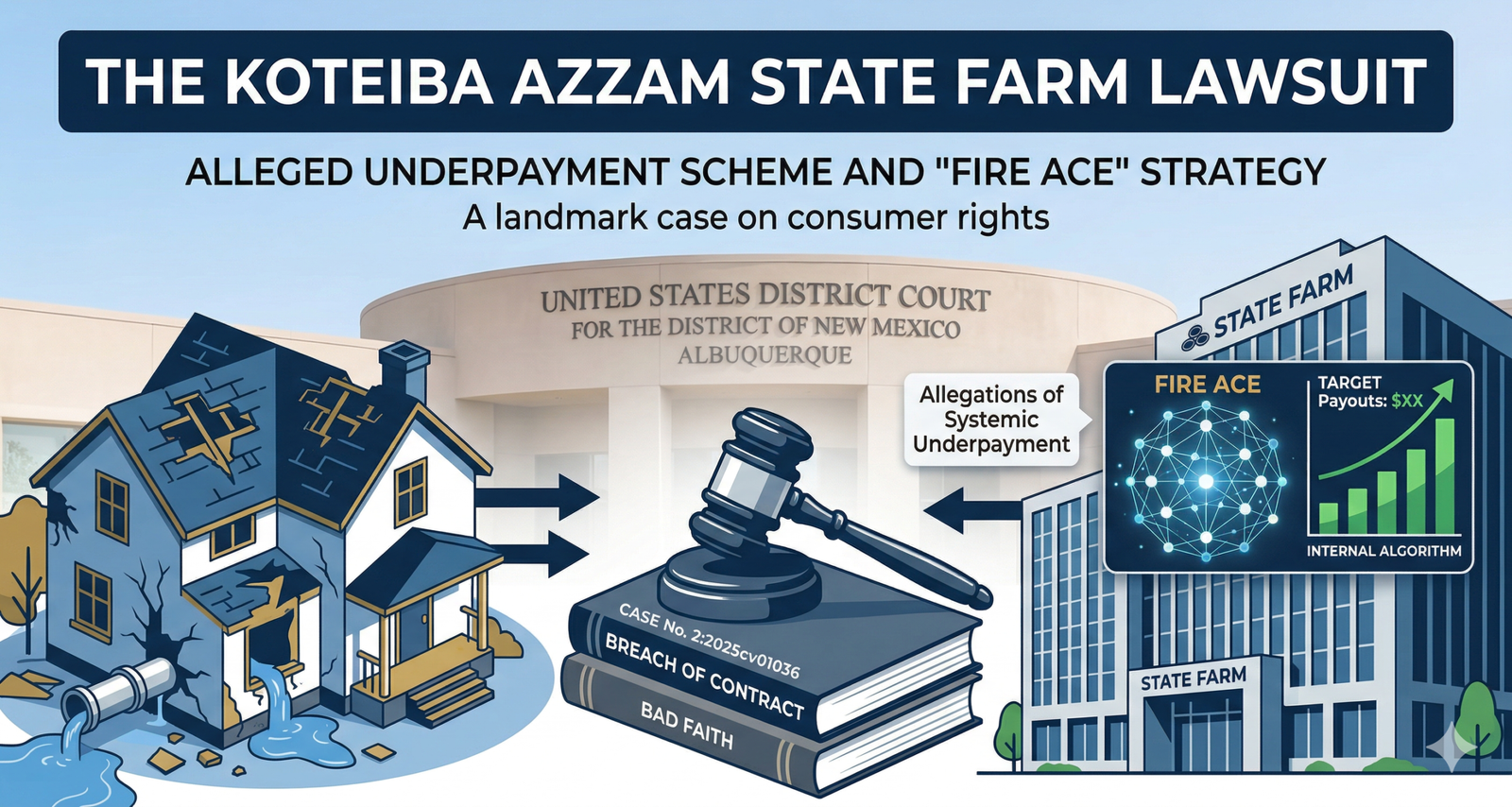

Koteiba Azzam’s federal lawsuit against State Farm Fire & Casualty Insurance Company represents a significant escalation in property insurance litigation, moving beyond a simple disagreement over repair costs to allege a calculated corporate scheme. Filed on October 19, 2025, in the U.S. District Court for the District of New Mexico (Case No. 2:2025cv01036), the complaint describes a profit-driven ecosystem that purportedly rewards the underpayment of claims and punishes policyholders who seek fair compensation.

Case Origins and the Sunland Park Incident

Azzam’s legal battle was sparked by a water damage event at his property in Sunland Park, New Mexico. After a pipe burst, causing substantial damage to the interior and the roof, a claim was filed with State Farm. Rather than receiving the “Good Neighbor” service advertised, Azzam alleges the insurer conducted a superficial investigation. State Farm reportedly closed the claim prematurely, refusing to cover essential repairs including a full roof replacement, leaving the residence in a state of disrepair.

Evidence presented in the complaint suggests that State Farm’s initial denial was not a mistake, but a test of the policyholder’s resolve. This practice, often called post-claim underwriting, involves searching for technicalities to limit payouts only after a loss has occurred.

The Architecture of the “Fire ACE” Program

Central to the Koteiba Azzam State Farm lawsuit is the Fire ACE claims management system. Azzam alleges that State Farm, working with the global consulting firm McKinsey & Company, redesigned its claims handling process to transform the department into a profit center. Under this model, the goal of a claims adjuster shifts from accurately assessing damage to meeting internal financial targets.

-

Algorithmic Valuation: Payouts are allegedly determined by preset software values rather than real-world market costs for labor and local materials.

-

Incentivized Denials: Staff adjusters and independent contractors are reportedly rewarded for maintaining low severity scores, which measure the average payout per claim.

-

Conflict of Interest: By incentivizing low payouts, the suit claims State Farm creates an environment where the adjuster’s financial benefit is directly opposed to the policyholder’s recovery.

Tactics of “Scorched-Earth” Litigation

Aggressive legal strategies are another pillar of the Koteiba Azzam State Farm lawsuit. Azzam describes a scorched-earth approach where State Farm purportedly uses its massive legal resources to make the cost of litigation higher than the value of the claim itself. This strategy serves a dual purpose: it wears down the individual homeowner and sends a deterrent signal to attorneys representing policyholders.

Policyholders who hire legal counsel may find themselves in a war of attrition. The lawsuit alleges that State Farm escalates these disputes regardless of the claim’s merits to demonstrate that challenging their decisions is a futile and expensive endeavor.

Legal Violations and Causes of Action

Attorneys Orlando R. Lopez and Danny Ray Scott have outlined multiple violations of state and common law in the Koteiba Azzam State Farm lawsuit. These counts aim to hold the insurer accountable for what they describe as deceptive business practices.

| Legal Count | Description of Allegation |

| Breach of Contract | Failure to pay for covered losses as explicitly stated in the insurance policy. |

| Bad Faith | Violation of the implied duty to act honestly and fairly toward the insured. |

| NM Unfair Trade Practices Act | Engaging in deceptive or unconscionable trade practices in New Mexico. |

| Common Law Fraud | Knowingly misrepresenting the terms of coverage or the necessity of repairs. |

Broader Industry Context in 2026

National scrutiny of State Farm has intensified alongside the Azzam case. Similar allegations have surfaced in other states, most notably in Oklahoma regarding the Hail Focus Initiative. In that instance, state officials investigated claims that the company used secret internal guidelines to deny roof damage claims that would have been covered under standard industry practices.

Class action movements are also gaining ground. In California, thousands of policyholders joined a suit alleging improper depreciation of sales tax in settlement checks. These collective legal actions suggest that the issues raised in New Mexico are part of a broader shift in how major insurers utilize technology and consulting strategies to manage their bottom lines.

Essential Steps for Policyholders

Homeowners facing similar claim denials can learn several vital lessons from the Azzam litigation. Managing a high-stakes insurance claim requires a proactive approach to evidence and communication.

-

Independent Documentation: Never rely solely on the insurance company’s adjuster. Hire an independent structural engineer or a licensed public adjuster to provide a competing estimate based on local market rates.

-

Meticulous Record Keeping: Create a detailed log of every interaction. If an adjuster makes a verbal promise or assessment, follow up immediately with an email summarizing the conversation to create a timestamped paper trail.

-

Demand Specificity: New Mexico law requires insurers to provide clear, written reasons for a denial. If the explanation is vague such as wear and tear demand the specific evidence or policy language they are using to support that conclusion.

-

Avoid Premature Settlements: Signing a release or accepting a “final” check before repairs are fully scoped can waive your right to seek additional funds later.

Current Status of Azzam v. State Farm

Presiding Judge Gregory J. Fouratt is currently overseeing the discovery phase in the U.S. District Court for the District of New Mexico. This stage is critical, as it allows Azzam’s legal team to request internal State Farm documents, emails, and Fire ACE training manuals. If discovery reveals that adjusters were pressured to meet profit quotas at the expense of policyholders, the case could trigger significant regulatory fines or lead to a massive class-action expansion.

Ongoing proceedings will likely continue throughout 2026. For the general public, this case serves as a landmark example of the tension between corporate efficiency and the fundamental promise of insurance: to provide a safety net when disaster strikes.